28 Jun 17

Property Outlook & Market Update Gibraltar 2016/2017

Market Update 2017

So on this latest issue, we get a little more serious and provide our annual “Market Update” which can also be accessed via our brand new website. We hope that the information provided will serve of some use in understanding the year gone by and what may lie ahead.

IN BRIEF

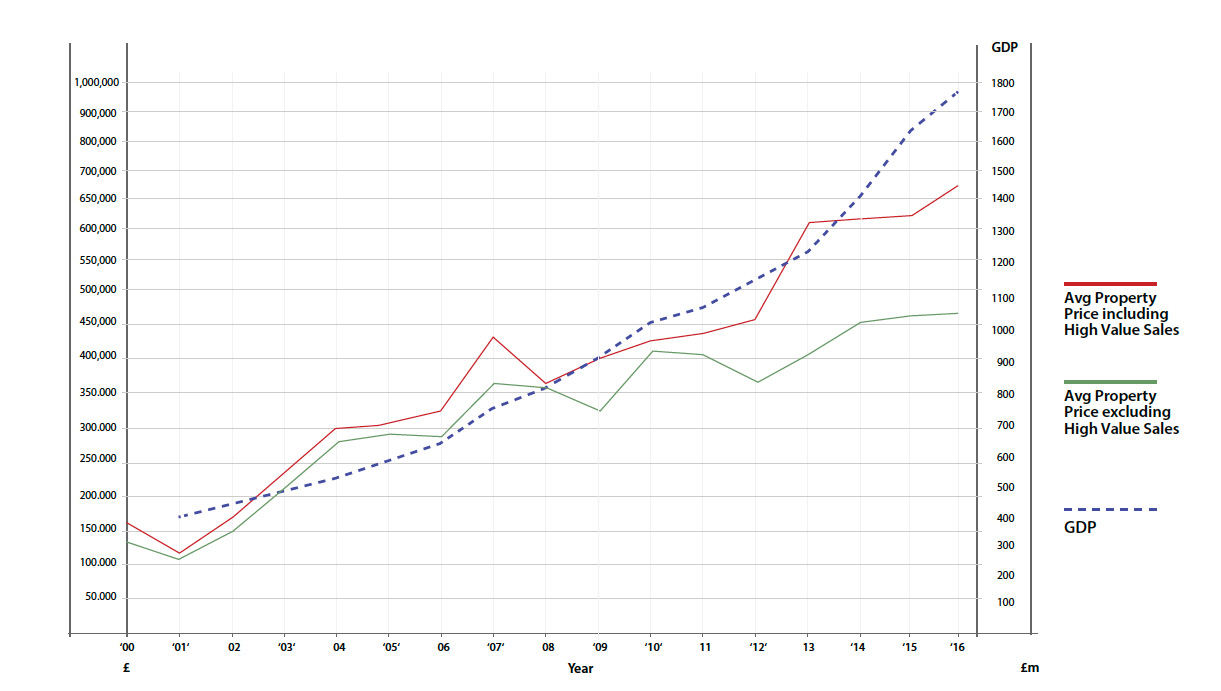

2016 was by no exception an interesting year to say the very least. We had forecast and expected the market to flatten somewhat (as shown by trend on the graph below). Given the exposure to off-plan sales as well as the fact that the market had grown substantially through the period from 2011/12 to 2013/14 of approx. 40%, the expectation of a somewhat flattened market with respect to prices was justified.

The impact of Brexit and the Referendum further compounded our thoughts, and the lead up to the 24th June 2016 was very much a slow train in terms of sales volumes. The result was wholly unexpected and at the time led to much speculation that the market would indeed arrest and see a 10-15% hit on values, as was being predicted in the London market. The reality was and has to date been an overwhelming shock.

The year 2016 can best be described as one of two halves, the first being one that most could have predicted, the second was unexpected, and delivered what from BMI’s perspective

resulted in one of the busiest 3rd and 4th quarters we have ever enjoyed. Why? In short, Gibraltar as we have said on so many occasions, continues to be a sanctuary to so many seeking a safe, well regulated, stable, low key jurisdiction. Yes, the uncertainty of Europe and the consequences of Brexit are unknown, but in light of the chaos surrounding us all, politically, economically and socially; Gibraltar remains a small beacon of security and prosperity.

On the 24th June 2016 I received an email from an international HNW client that in our view underpins and articulates what in fact seems to be unfolding from a Gibraltar Inc perspective – it read as follows:

“My belief in Gibraltar’s strength, especially in its entrepreneurship and government convinces me that as soon as we shake off the inevitable sense of disappointment we will start to see that there is no shortage of opportunities for this small but dynamic country”.

The data in respect of “average house price excluding high value properties” were generated by excluding the highest valued 10 per cent of properties sold by BMI in each respective year. NB. Note that the GDP graphic has no direct bearing or correlation to the information provided on average property prices and is purely an indicator with regards to trends.

WHAT’S IN STORE FOR 2017?

SALES/RESIDENTIAL

• Our portfolio: remains one of the largest and most updated on the rock. Volumes have been increasing and will inevitably increase further due to the various off-plan developments soon to come to market, and where certain numbers of speculators will feed their investments into the mainstream – the key point of interest will be what impact this will have on prices? So far prices have levelled with slight increases and remain steady. We expect our portfolio to see further listings over the year 2017.

• Prices: 2016 as shown on our graph shows a price increase across the board of approximately 8%, with our average price guideline excluding high value sales showing an increase of approximately 4% throughout the year. Due to some unexpected high value sales, which were out of the norm, we would prefer to suggest that the real average increase over the year was in the region of 5%. Given uncertainties surrounding the Brexit situation it is hard to predict or indicate market trends for 2017. At this stage we can only be encouraged by the almost perverse activity experienced during the latter half of 2016 which saw our sales numbers break all previous records for Q3/4. As this update goes to print we are delighted to confirm that the first two months of 2017 have seen a continuation of this buoyant trend.

(Please see section under “Economy” for our thoughts on themarket ahead and the impact on prices)

• Off-plan sales: in total, there are approx. 450+ units underconstruction over various developments. The first large scale scheme to be completed will be Midtown phase 1 which is scheduled for Nov 2017 followed by Ocean Spa during mid- 2018 and Quay 29 circa end of 2018. Others will follow during 2019. The position with respect to re-sales so far is positive. We have always kept a watchful eye on speculative market and the impact on an oversupply of re-sales due to this. To date we are positively encouraged by the fact that the few (executed) re-sales converted in recent months have delivered approx. 10% increases on sales values and up to 35% on the instalments paid by initial option holders. This in our view is a strong indicator of a growing confident market so far.

Our view and forecast for 2017 is uncertain, given external affairs relating to Brexit and the impact that this may have on Gibraltar from a political and economic perspective. Indications are that Gibraltar could benefit from the uncertainties in Europe but particularly the chaos and instability throughout European economies.

On this basis, our opinion is cautiously siding on a real prospect that prices will certainly hold at current levels and may see further growth in certain sectors similar to that in 2016 of circa 5%.

Off-plan re-sales will, in our opinion, be a good indicator of confidence or lack of and our focus will be on assessing whether or not the market has over-exposed itself to weak speculators, and which developments may be more adversely affected by this. As mentioned above, we have already seen a strong indicator that re-sales in certain developments are seeing margins of up to 15%. (Please contact us for further information on this).

Our thoughts on a developing 4 tier market (low, mid, high, ultra-high) as described over the past 36 months are now firmly accepted. We believe that this more than serves as a positive indicator of the potential that the market continues to enjoy. The very fact that we are attracting a new ultra-high segment is the clearest sign of confidence from a new emerging market.

2016 saw our involvement in the sale of the 1st of The Sanctuary Villas to be sold, with a great many applicants and clients expressing their belief in our prospects ahead. This reassures us that, regardless of uncertainties in the market as described within this update we continue to see a great margin in this internationally driven sector.

LETTINGS

Our property management portfolio has grown substantially since we began to focus in this sector back in 2006; we now have over 120 properties under management. The market has been buoyant since 2011, which in fact, we had indicated would be the case and would continue to be so; however, 2016 and in particular Q3&4 has been exceptional in terms of volumes of properties let and thereby rendering the market to the lowest point in supply since 2000.

We have always indicated and suggested that this may see a prelude to rising prices as was the case in 2000 and we believe that existing new letting entrants, will translate into new purchaser applicants.

Increases in lettings prices (as has been the case) are driven by demand, but are also good indicators of economic activity. Due to the delivery of new developments and a supply of properties on to the market over the coming 12-18 months we do not necessarily see this approach this time round and take a view that rental prices are more likely to remain settled, certainly leading up to the completion of the recent new “off-plan” schemes.

Landlords will no doubt be pleased to see their existing ROI doing well across the board and gross yields generally ranging between 4.5%-6.0%. We expect this to remain the case over the next 12 -18 months.

CHIEF MINISTER’S ANNOUNCEMENT

Parliament 08.07.16

“I announce a new budget measure today that where any property is constructed in the next thirty months from the 1st July 2016 and that property is rented for residential purposes, the owner of that property will receive a tax credit equal to the tax payable on the profits earned on the first twentyfour months of rent occurring in the first five years after the completion of construction of that property. The tax credit is not refundable and can be offset against the tax payable to extinguish any liability to tax.”

COMMERCIAL

The past 18 months have seen significant proposed office developments launched to market. World Trade Centre and Midtown are the main players and both account for approx. 27,000sqm of new grade A office space. Both schemes are scheduled to be completed by early 2017 / late 2017 respectively.

Aside from the above we are also seeing the re-development of various Freehold Town Centre buildings converted and re-fitted into HQ offices for particular users.

Demand has clearly increased with the additional pressure of there being no new build in this sector for quite a number of years. Our views (last year) on whether there is real demand to meet the forecasted sqm being proposed were met with an element of caution given the substantial schemes in the pipeline. Completion of WTC has very clearly underpinned the fact the market has indeed welcomed this grade A office project with over 90% let.

It is fair to say, however, that over the past 36 months there has been a clear demand and outcry by the various economic sectors, namely Gaming, Insurance and Financial Services and the general market as a whole, for new upgraded 21st century office accommodation. These demands will most certainly be met.

With respect to current availability / stock, it is safe to say that there are options in various locations, particularly in older commercial developments. The offering is generally lower quality and in certain areas, compromised in terms of layout flexibility and sizes.

Moving forward; we take the view that there will be an element of decanting from the older commercial properties into the newer and better designed office schemes. Worthy of note is the fact that letting rates/sqm have not been compromised at the higher end due to the decanting, but in fact are maintained at the highest levels to date which further suggest that applicants are prepared to pay high end prices for high end specs. In our view this creates an opportunity for landlords with older (decanted) buildings, to upgrade their commercial properties, in line with 21st century requirements.

Fundamentally it will be the ability of the economy to grow further and attract new business, which we believe Gibraltar will continue to do. We take the view that new modern office options will only serve to improve the commercial offerings in the market and will generate new business.

NEW DEVELOPMENTS

2015 saw the launch of Midtown phase 2, Ocean Spa and Kings Wharf Quay 29. In brief all three phases / developments sold out in no time with only a few properties remaining directly from the developer. Although one would be tempted to mark this as a huge success on the part of the developers, we will keep a watchful eye on where demand for these units has originated from and who the buyers are.

Re-sales have started to materialize and to date, we encouraged by the fact (as mentioned in previous sections above) that resales are seeing uplifts of up to 10% of purchase prices held by option holders.

We have always maintained that a mix of owner occupiers, seasoned investors and a small measure of speculators is healthy, any overdose of the latter and you become exposed – to learn more about our thoughts on this, please feel free to call us.

We reserve our position on how we see this evolving throughout the year in light of political matters surrounding the Brexit negotiations.

ECONOMY

Although we prefer to refrain from commenting on economic activity, we have found it useful to refer to the GDP figures (blue dotted line on graph) in order to indicate economic strength or weakness, which is a main driver in property values. 2016 continued with much the same progress as the previous year and a projected growth of +7.5%. Brexit remains very much on all our minds and muddies the waters with regards to any forecasting on how the economy will unfold over the coming 12-24 months.

The current climate however, and if one can ignore the Brexit factor, in our view continues to be very positive and likely to grow sensibly. For six years (since 2011) we have witnessed the market harden up and prices rise, 2013 underpinned this further with a marked increase in “high value” sales which, as seen on the graph marks the beginning of the fourth tier sector in the market which we have referred to in the tables above.

Property values have flattened slightly over the past 24 months from the previous four years and have not mirrored GDP growth as in the past; it would be unrealistic to expect as much. We see this settling as a breather in the market, which in essence allows stakeholders to measure and assess what may lie ahead. Our take very much depends on new business for Gibraltar, but more importantly the ability for our economy and financial services sector to continue to strive, compete and attract new entrants from other jurisdictions. We also believe that the private client space will feature highly over the next few years as we see high value clients looking for jurisdictions that can afford them a safe, proactive, low tax and regulated environment.

KEY FACTORS OF NOTE:

- Our lettings portfolio today stands at an average of 8 units, a marginal decrease from last year and very lowcomparably from an all-time high of 40 units 7 years ago. Demand is high – supply is low!

- Our sales portfolio is at an average of 125 units for sale from an all-time high of 240 units 7 years ago.

- Our sales volume in 2013/14 saw a 5% increase with 2014/2015 increasing further to approx. 15% from the previous year (not including off-plan sales). 2015/2016 has seen further increase of 10% indicating a positive buoyant market.

- High Value market sales are here to stay long term underpinning the top end of the market and the confidence from applicants in this sector. Sales at Buena Vista Park and The Sanctuary are evidence of this.

- New Developments (residential) launched from 2014/15 amount to approx. 450 units (not including Govt housing schemes) with forecasted completions of 2017 – 2019.

- GDP growth (forecasted figure) for 2016 is +7.5%.

KEY RELATED ECONOMIC FACTORS:

- There continue to be NO bank repossessions.

- Unemployment remains below 1.5%.

- Finance industry continues its organic growth, with exciting new ventures already inbound boding well for the future.

- Gibraltar remains the only highly regulated, low tax, English speaking centre in Europe.

The information provided in this Market Update is for informational purposes only. BMI Group endeavours to ensure that material contained in this Update is accurate and complete at the date of publication; however it does not guarantee the accuracy or completeness of the information, including photographs, text, graphics, renderings and other items contained herein. You should further recognise that information contained may become out of date at any time. All prices, features, specifications, plans, availability, statistics, graphs, charts are for informational purposes only and are subject to change without notice.

No warranty (whether express or implied) of any kind and no responsibility is assumed for the owners or operators of or content in any of its content and shall not accept any liability, loss or damage of any kind arising from any inaccuracy or omission in or use of your reliance upon any information contained herein. Readers are to rely solely on their own due diligence.